The Roads To Hyperbitcoinization: Describing The ‘Transition Agents’ Bringing Us

This article is the second part in a series where we outline the views and predictions made by the Bitcoin community concerning the prospect of hyperbitcoinization. In our analysis, we highlight “transition agents”: main players, groups of players or institutions that could accelerate the transition to a Bitcoin world. For each topic, we base our arguments on the references collected, and if possible, present data that aims to assess the probability of this outcome.

The first article described top-down scenarios initiated by institutional agents or governments whose influence is expected to trickle down to a wider audience. We identified monetary inflation and the rollout of central bank digital currencies (CBDCs) as probable scenarios initiated by central banks, while bitcoin hoarding, a rise in cross-border payments in bitcoin, bitcoin as a legal tender and even the advent of a hash war were identified as scenarios likely to induce government acceptance of Bitcoin. In view of the recent pronouncement by El Salvador, it appears that political agendas in South America are in a state of flux, in particular in countries with national elections scheduled for 2021 and 2022.

This second article aims at understanding of bottom-up type initiatives carried out by businesses, communities and individuals.

Bottom-Up Scenarios

We identified several notable hyperbitcoinization scenarios that emanate from two large groups of actors. The first group represents private-sphere-led initiatives brought together by established firms and startups. The second group is composed of grassroots initiatives mostly impulsed by the Bitcoin community whose main purpose is to educate and help new users to be onboarded. The article begins with a discussion of the initiatives driven by these two groups before turning to an examination of emerging individual behaviors. In this article, we have followed the principle of methodological individualism, well-known in the Austrian school of economics, which consists in explaining large-scale social phenomena based on subjective individual actions and motivations.

Private Sphere

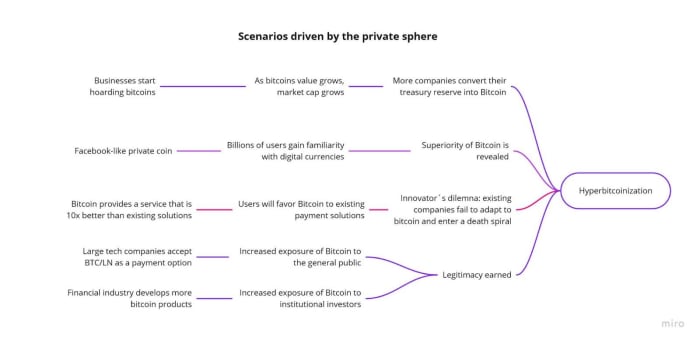

Figure one depicts scenarios initiated by private actors that could — intentionally or unintentionally — set off a chain of events driving to hyperbitcoinization.

Figure one: Chain of events driven by private actors.

Business Adoption

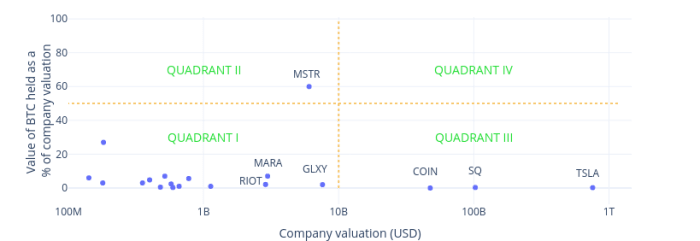

Since inception, Bitcoin has demonstrated that it offers a wide variety of benefits to users. Its value proposition as a safe haven for individuals is without question one of its key enduring narratives. In August 2019, the world was surprised when MicroStrategy (MSTR), a NASDAQ-listed public technology company, announced that it was converting part of its cash reserves into bitcoin. Figure two depicts publicly-traded companies that reported owning bitcoin on their balance sheets or have converted a fraction of their cash reserves to bitcoin over time.

Figure two: Mapping of U.S.-based public companies owning bitcoin (Q2 2021). Source: cryptotreasuries.org.

To date, we can divide this trend into four distinct areas:

- Quadrant I is composed of early-adopter companies that have held bitcoin for several years. It includes Bitcoin mining companies (GLXY, MARA, RIOT) that, historically, have bet on the long-term appreciation of the asset. As they grow, these companies will naturally move into Quadrant II.

- Quadrant II is territory personified by MicroStrategy, which has suddenly converted a large part of its reserves denominated in USD into bitcoin and keeps on purchasing more bitcoin recurrently. The company value seems to be strongly correlated with its bitcoin holdings (60%).

- Quadrant III contains the innovators: companies like Tesla and Square (now Block) that have converted a relatively small fraction of their reserves into bitcoin and may increase their exposure in future.

- Quadrant IV is probably not reachable for most companies. It would imply large companies with valuation exceeding $100 billion getting more than 50% of their reserve in bitcoin. If it happens, the amount of capital allocated into bitcoin will approximate trillions of dollars.

Since the MicroStrategy announcement, many other companies have started to display an interest in Bitcoin, and we can expect to see more of these kinds of initiatives appearing over the coming months once decision-makers have weighed their choices.

If hyperbitcoinization comes to fruition, the revenues, costs, profits and valuations of all companies could be accounted for in bitcoin (Mimesis Capital and Burnett), and most valuable companies would be the ones holding the largest chunks of bitcoin on their balance sheet.

Private Coin

When Meta (formerly Facebook) announced in 2019 that it would be launching a new digital currency, Diem (originally called “Libra”), the move caught governments and financial institutions alike off-guard. Diem’s stable value was to be derived from a basket of fiat currencies (U.S. dollar, euro, Japanese yen, British pound and Singaporean dollar) that would allow any Facebook user to send money as easily and intuitively as sending a message.

Although an appealing idea in many ways, concerns were raised in some quarters about trusting a company that feeds on user data. Some feared Diem would embody the worst of monies and data privacy practices. On the other hand, the launch of a private digital currency like diem may serve to familiarize large numbers of users with this emerging technology and thereby act as an on-ramp to broader Bitcoin adoption. As users get acquainted with digital currencies, they will develop an understanding of bitcoin as a scarce, censorship-resistant and decentralized digital money.

10x Factor

Bitcoin is often considered a better form of money because it combines significant improvements in terms of portability, divisibility or fungibility when compared to both past and present forms of monies, along with bringing radical disruption in terms of resistance to censorship and fixed supply. One aspect that remains underexplored is transaction costs on the economy.

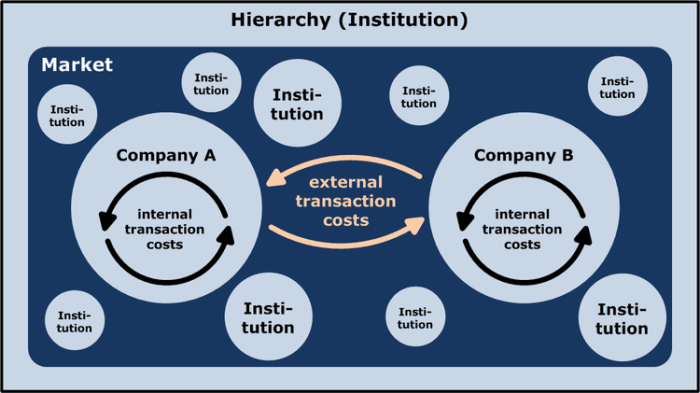

Over the centuries, people have cooperated to minimize transaction costs and produce more efficiently what they are unable to produce individually. The theory of the firm by Ronald Coase describes the relationship between internal and external costs.

Figure three: Impact of transaction costs on dynamics of growth. Source: Wikipedia.

When a firm’s external transaction costs are higher than its internal transaction costs, the company will grow. If the external transaction costs are lower than the internal transaction costs the company will downsize by outsourcing, for example.

Applying this theory to the banking sector, we can project that the Bitcoin protocol is likely to capture a significant portion of the banking industry value proposition, and it is not hard to imagine that it could probably capture it entirely once the Bitcoin stack becomes a more tangible reality (see figure three). Over time, we can expect the value created on top of the Bitcoin stack to first capture the value of the financial industry, and then surpass it.

If the transaction costs incurred by Bitcoin users are lower than transactions enabled by conventional payments rails, demand will shift to the cheaper channel. Following Brexit, Visa and Mastercard increased their interchange fees by almost 1%, squeezing merchants’ bottom lines even further. This has also occurred in Colombia, where merchants stopped using debit and credit cards to avoid the excessive fees.

Elsewhere, merchants who want to reduce interchange and swipe fees, may also consider other payment options such as the Lightning Network as a means of reducing costs. Payment service providers risk entering a death spiral initiated by a shrinking customer base placing pressure on profit margins and ultimately rendering their services less competitive. In the context of increasing compliance costs in the banking and payment industries, the likelihood…

Read More:The Roads To Hyperbitcoinization: Describing The ‘Transition Agents’ Bringing Us